EU taxonomy

As part of the 2015 UN Climate Change Conference, the Paris Climate Agreement with the objective of achieving climate neutrality by 2050 was set. In order to achieve this goal, the EU has drawn up the "Financing Sustainable Growth" action plan. The EU taxonomy is a core component of this action plan and is intended to contribute to the sustainable transformation of the economy.

Initially, only large listed companies with more than 500 employees were affected by the EU taxonomy, but this circle has now been extended with the entry into force of the Corporate Sutainability Reporting Directive (CSRD).

With the introduction of the EU taxonomy, the EU provides a classification system that enables the identification of ecologically sustainable economic activities and also creates the basis for a uniform understanding of sustainability.

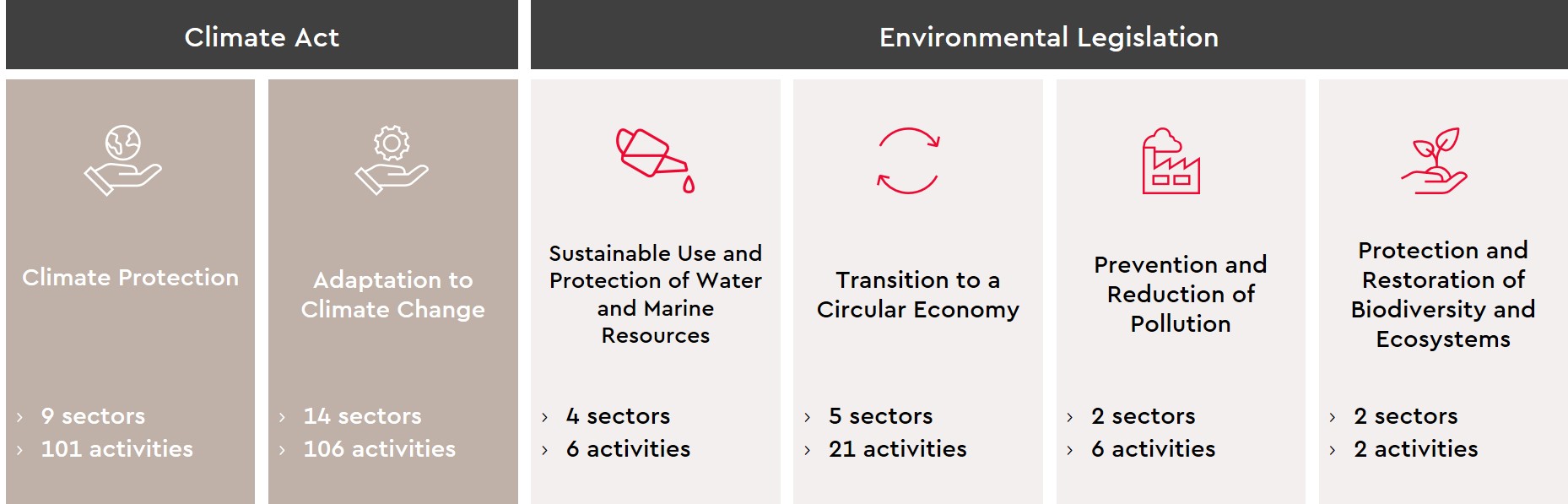

The classification system is based on six environmental objectives defined in the EU Taxonomy Regulation. With these six environmental objectives in mind, the EU has adopted two delegated acts (Climate Law Act and Environmental Law Act), which serve as the basis for identifying environmentally sustainable economic activities:

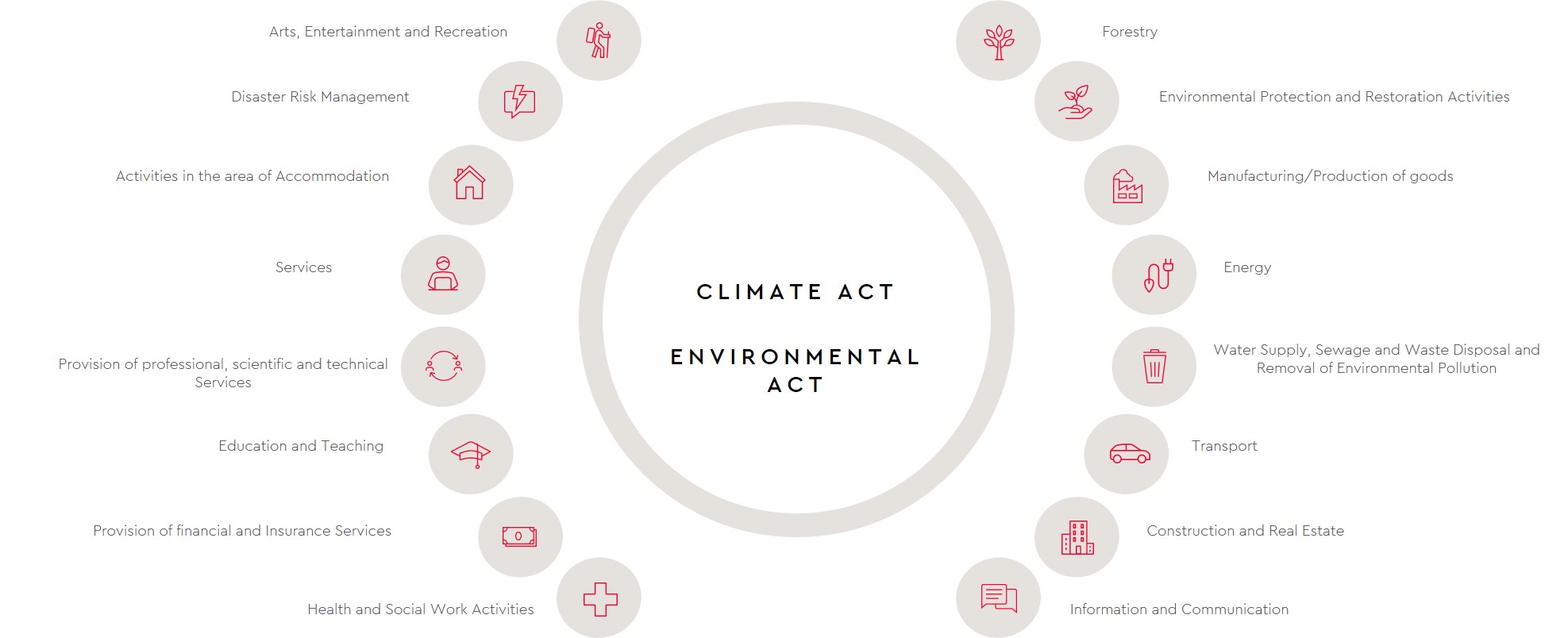

The EU taxonomy currently contains over 240 economic activities, which are classified in the legal acts according to environmental objectives and cover a total of 16 sectors:

If an economic activity is listed in one of the delegated acts, it is taxonomy-eligible, i.e. potentially environmentally sustainable within the meaning of the EU taxonomy.

Take a detailed look at the sectors and economic activities in the EU Taxonomy Compass here.

However, it should be emphasized that no economic activity per se can be classified as sustainable in the sense of the EU taxonomy. Several conditions must be met for an economic activity to be considered environmentally sustainable or taxonomy-compliant.

The focus here is that an economic activity must make a significant contribution to one of the environmental objectives while at the same time not compromising any other environmental objective. To ensure this, the EU has defined so-called technical assessment criteria for each economic activity taken into account in the delegated acts. Companies must therefore check and fulfill these criteria in order to be able to declare a sustainable economic activity within the meaning of the EU taxonomy.

In addition to the evaluation of taxonomy conformity, certain quantitative and qualitative information must be disclosed. This includes information on the taxonomy process in the company on the one hand and the disclosure of the key figures sales, capital expenditure (CapEx) and operating expenditure (OpEx) [including the corresponding taxonomy-compliant and taxonomy-compliant portions] on the other hand.

In addition, companies must provide evidence of compliance with the minimum safeguards. The requirements are essentially based on the OECD Guidelines for Multinational Enterprises, the United Nations Guiding Principles on Business and Human Rights and the International Bill of Human Rights.

Large listed companies were required to disclose both the taxonomy compliance and taxonomy conformity of their business activities for the first time for the 2022 financial year. We have aggregated the taxonomy data of the DAX and MDAX companies in a taxonomy dashboard.

Make various comparisons by navigating through our taxonomy dashboard and setting appropriate filters. Click here to go to our dashboard.

Although there are essentially three steps, the complexity and time required to implement the EU taxonomy in a company should not be underestimated. Companies must break down key financial figures [such as turnover] into environmentally sustainable economic activities, i.e. financial and non-financial information must be linked.

The requirements resulting from the EU taxonomy pose new challenges for many companies. On the one hand, the technical implementation must be emphasized here, as IT and process landscapes in the company must be adapted to enable reporting in accordance with the EU taxonomy. On the other hand, examining the content of the technical assessment criteria is also challenging, as this requires technical expertise from a wide range of areas [and interdisciplinarity].

Our interdisciplinary team will be happy to support you in implementing the requirements arising from the EU taxonomy. We work with you to develop a tailor-made consulting approach.

Please do not hesitate to contact us if you are interested or have any questions.

Your contact to us

Do you have any questions about our services or WTS Advisory? We look forward to your message or your call!